One for the Gold Bugs – Are we seeing a structural change from Au’s renaissance?

Evan Lucas

22/11/2024

•

0 min read

Share this post

Copy URL

There's been plenty made this year about gold's incredible rise to new record levels. A point that gold bugs love to point out. As we sit here gold is trading at around US$2700oz having reached an all-time high that was just shy of US$2900oz.

Thus the question has to be asked: where is the limit? And where too from here for the inert metal? The movements over the last five years clearly suggest there is a structural change going on inside the very definition of what gold is. 14.7% in the last six months. 29.4% year to date. 34.2% in the last 12 months A staggering 82.3% in the last five years.

That is telling a story that is different to the original fundamentals we were taught at university and then as fundamental traders. Let's look at that theory: gold usually trades closely in line with interest rates, particularly US treasuries. As an asset that doesn't offer any yield it typically becomes less attractive to investors when interest rates are higher and usually more desirable when they fall.

That still technically holds true, However what has changed is how much central banks are interfering with that fundamental. Since 2022 when Russia invaded Ukraine one of the main reactions from the West was to freeze Russian central bank assets. Since that point the Russian central bank particularly has been buying gold as a form of asset store/reserve.

It has also allowed it to avoid the full force of financial sanctions placed on it. But they're not the only ones doing this; emerging market central banks have also stepped up their purchasing of gold since this sanction was put in place and are rapidly increasing their own central bank reserves. Then we look at developed markets central banks.

The likes of the US, France, Germany and Italy have gold holdings that make up to 70% of their reserves are net buyers in the current market. That suggests something else is afoot. Are they concerned about debt sustainability?

Considering the US has $35 trillion of borrowings which is approximately 124% of GDP, do central banks around the world see risk? Considering that many central banks have the bulk of their reserves in US treasuries coupled with the upcoming unconventional administration in the Oval Office this certainly puts gold’s safe haven status in another light. There are truly unknowns with the upcoming trump administration and gold is clear hedging play against potential geopolitical shocks, trade tensions, tariffs, a slowing global economy, deft defaults and even the Federal Reserve subordination risk So what is the outlook for Gold over the coming years and just how high could it go?

Consensus over the next four years is quite divided: by the end of 2024 the consensus is for gold to be at US$2650oz and then easing through 2025 to 2027 to $2475oz. However there are some that are calling for gold to reach the record reached in September this year before surging towards $2900oz the end of 2025 and holding at this level through most of 2026. And right now who could blame this prediction - Gold bugs believe the confidence in gold’s enduring appeal amid a volatile macroeconomic and geopolitical landscape is a bullish bet.

Expectations for sustained diversification and safe-haven flows do appear structural and with central banks and investors seeking to mitigate risks in an environment characterised by persistent uncertainty, geopolitical tensions, and economic volatility. And it's more than just the demand side that's leading the charge. The supply side of the equation further supports our bullish outlook.

Gold mine production is inherently slow to respond to rising prices due to long lead times for exploration, development, and production ramp-up. Furthermore, major producers avoid aggressive hedging strategies, as shareholders typically prefer full exposure to gold’s upside potential. The supportive fundamental backdrop reinforces that demand from both the official sector and consumers will remain robust, while supply-side constraints provide a natural tailwind for price appreciation.

What we as traders need to be aware of is many investors actually believe they've missed the rally and are wary of buying gold at all-time highs. There are some that believe gold is due pull back even a correction as they struggle to make sense of gold in the new world. The divergence away from yields coupled with unknowns out of China and the US has made them nervous to buy this rally.

But we would argue the pullback has probably already happened. If we look at the gold chart, since the US presidential election gold has moved through quite a reasonable downside shift. Dropping from its record all time high to a low $2530oz.

That decline has clearly been cauterised and the momentum now is clearly to the upside. We can see from the chart that spot prices are now testing the September-October consolidation period. Any clean break above these levels would see it going back to testing the head and shoulders pattern at the end of October-November.

This will be the keys to gold for the rest of 2024. But whatever happens in the short term the long-term trend suggests there is more for the gold bugs to delight in.

By

Evan Lucas

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs.

Sebuah berita utama tentang peradaban yang “sekarat malam ini” dibangun untuk membanjiri, tetapi sinyal yang lebih jelas mungkin adalah ketenangan di bawahnya, karena pasar mulai memperlakukan siklus eskalasi tajam ini diikuti oleh de-eskalasi mendadak sebagai pola, bukan kejutan.

Dalam lingkaran makro, pola itu memiliki label tumpul: TACO, atau “Trump Always Chickens Out”. Frasa dimuat, tetapi logikanya sederhana. Ancaman tekanan maksimum melanda, aset berisiko goyah, kemudian jeda, penundaan atau hasil yang lebih lembut muncul begitu biaya ekonomi mulai menggigit.

Itu tidak berarti risikonya kecil. Ini mungkin hanya berarti investor telah terbiasa dengan naskah di mana retorika berkobar, pasar menyerap guncangan, dan pengekangan muncul sebelum skenario terburuk sepenuhnya muncul.

Developing situation

|

Strait of Hormuz | Section 122 Tariffs

PublishedApril 2026

Brent CrudeAbove US$100

VIX31

In focus6 markets

Oil PositioningDecade-low longs

The Framework & MechanismIs the market the red line?

+

This is where the TACO idea starts to matter. Traders are not just watching the rhetoric. They are watching when it starts to hit markets, inflation and the wider economy.

Oil is at the centre of that risk. If disruption around the Strait of Hormuz starts to threaten global energy flows, the story quickly becomes macro. Higher oil can lift inflation expectations, pressure central banks and tighten financial conditions.

That is why a pause can look less like diplomacy and more like pressure relief. The real red line may be the point where the economic damage becomes too obvious to ignore.

Short Squeezed

Positioning adds another layer. Oil still looks under-owned, with futures positioning near decade-long bearish extremes. If a fresh shock lands, short-covering could drive prices higher much faster than fundamentals alone would suggest.

That is the short-squeeze risk. In the Commitment of Traders (COT) report, recent data suggests oil long exposure is relatively low by historical standards.

Humanitarian Reality

Whatever may be promised in political messaging, any sustained conflict in Iran would carry a heavy cost in displacement, infrastructure damage and wider regional stress. A relief rally in markets does not change that.

Global Isolation

Even if pauses are used to steady domestic market sentiment, allies and multilateral institutions may view bluff-and-retreat tactics as a credibility problem that creates longer-term diplomatic friction.

Positioning gap indicator

Divergence analysis between positioning and risk environment

APRIL 2026

Bars show GO Markets’ internal estimate of the divergence between current futures positioning and levels seen in comparable historical shock environments.

Brent crudeExtreme

Gold (XAU/USD)Very high

Nasdaq 100High

USD/CNHHigh

US 10 yr yieldMedium

USD/CADMedium

Extreme decade scale positioning extreme

High significant divergence

Medium moderate divergence

Methodology note

The Positioning Gap Indicator is based on GO Markets’ internal analysis and is intended as a high-level, illustrative framework only. It uses a combination of market positioning data, historical comparisons and discretionary assumptions about how similar energy and trade shocks have affected markets in the past. The ‘Extreme’, ‘Very High’, ‘High’ and ‘Medium’ labels are relative internal classifications, not objective market standards, and should not be relied on as predictions, forecasts or a guarantee of future outcomes.

The Six Markets

The six markets that matter most

Each of these six markets is exposed to the current situation through a different mechanism. Understanding the mechanism, not just the price, matters. It helps explain whether a move is a headline reaction or the start of something broader. Tap any card to expand the full analysis.

01

BRENT

Brent crude oil

ENERGYDIRECT CHANNELSQUEEZE RISK: EXTREME

+

The Clear Transmission Channel

Brent is the international benchmark for crude and the most direct transmission mechanism in this geopolitical thesis. Any disruption to physical flows, particularly through the Strait of Hormuz, forces an immediate tightening of global energy supply.

The Positioning Backdrop

Futures positioning currently sits at a ten year bearish extreme. Leveraged funds have cut long exposure heavily. In the event of a physical supply shock, this imbalance creates the potential for a violent short covering squeeze.

● Bull Case

Hormuz disruption extends beyond four weeks. Extended disruption could lift Brent sharply if supply flows are impaired for longer.

● Bear Case

Diplomatic intervention reopens the strait quickly. Strategic petroleum reserve (SPR) releases and increased spare capacity cap any price rally.

Strategic Marker

US$120: the point at which energy inflation becomes a direct Federal Reserve policy problem, rather than just a market narrative.

02

XAU/USD

Gold

SAFE HAVENUNDER-OWNEDSQUEEZE RISK: VERY HIGH

+

The Counter-Intuitive Setup

Despite a clear geopolitical risk profile, leveraged funds have been reducing bullish gold exposure. This leaves the market under-owned at the exact moment the fundamental case for safe haven assets is strengthening.

The Inflation Variable

The critical factor for Gold is whether energy-driven inflation limits the Fed's room to maneuver. If policy flexibility weakens, Gold could catch up quickly as a hedge against stagflation.

● Bull Case

Real yields fall as energy inflation outpaces rate hikes. Under-owned positioning amplifies the catch up move as institutional funds rebuild exposure.

● Bear Case

Geopolitical tensions ease rapidly. The Fed remains credibly focused on inflation, keeping real yields positive and supporting the USD over Gold.

Strategic Marker

One level to monitor is prior resistance, alongside any change in COT positioning.

03

US100/NAS100

Nasdaq 100

TECHNOLOGYDUAL PRESSURERATE AND SUPPLY RISK

+

Why it is a complicated position

The Nasdaq faces immediate pressure from two fronts: Stickier energy-driven inflation forces rates higher for longer, compressing multiples, while trade tensions unsettle the supply chains beneath major tech names.

Why the 10 year yield matters here

When the 10 year Treasury yield holds above 4.5%, the future value of technology earnings must be discounted at a higher rate. AI linked earnings momentum must overpower this valuation headwind.

● Bull Case

Earnings season delivers proof of AI investment generating real revenue. Index components successfully insulate supply chains, and AI capex momentum overrides the macro headwind.

● Bear Case

Energy inflation keeps yields above 4.5%. Multiple compression in high valuation names triggers a broader index decline amid disappointments in AI monetization.

Strategic Marker

S&P 500 at 6,498: a widely watched Fibonacci cluster. A sustained move below this threshold highlights a historically challenging framework for growth equities.

04

USD/CNH

US dollar/offshore Chinese yuan

FXBEIJING READPOLICY PROXY

+

What it tells you

USD/CNH is the cleanest real time read on how Beijing is responding to tariff pressure. A sharp rise suggests China is allowing currency weakness to absorb the costs of trade friction.

Why it matters beyond China

A move in USD/CNH doesn't stay contained. It spills into Asian equities, commodity demand, and broader risk appetite. Deliberate depreciation signals a shift in the global trade environment.

● USD Bull / Yuan Bear

Beijing allows yuan weakness as a deliberate countermeasure. Capital outflows accelerate, and USD safe haven demand reinforces the move.

● Yuan Recovery

Trade negotiations begin and a face saving off ramp is found. PBOC intervention defends the yuan, and the dollar's safe haven premium fades.

Strategic Marker

7.30 on USD/CNH: a sustained move above this has historically been associated with broader risk off moves in Asian markets.

05

US10Y/TNOTE

US 10 year Treasury yield

RATESMACRO PLUMBINGSHAPES EVERYTHING ELSE

+

Why it sits under everything

The 10 year yield shapes mortgage costs, corporate borrowing, and the valuation framework for risk assets globally. When it rises, borrowing becomes more expensive across the entire system.

The Independent Movement Risk

If oil forces the Fed to delay cuts, the 10 year yield could rise regardless of Fed communication. It can tighten financial conditions even before a formal policy shift occurs.

● Rates Fall Case

Oil shock proves transient. Fed maintains guidance and 10 year yields pull back toward 4.0%, relieving pressure on equities and providing support for bonds.

● Rates Rise Case

Sustained oil above US$100 pushes inflation higher. Fed pauses rate cut language and the 10 year yield breaks above 4.5%, compressing equity multiples.

Strategic Marker

4.5% on the 10 year yield: a sustained break above this while oil remains above US$100 is a historically challenging combination for equities.

06

USD/CAD

US dollar/offshore Canadian dollar

FXOIL-LINKEDLEAD INDICATOR

+

The Double Exposure

USD/CAD is a lead indicator because Canada sits at the intersection of energy and trade. It benefits from higher oil revenue but is highly sensitive to US economic and trade conditions.

When the Forces Collide

When oil rises, the CAD often strengthens; when trade stress rises, it weakens. In the current environment, these forces are colliding rather than canceling each other out.

● CAD Strengthens

Oil sustained above US$100 boosts export revenue while trade tensions stay short of Canada specific tariffs. Bank of Canada holds rates steady.

● CAD Weakens

Safe haven USD demand outweighs the oil benefit. Bank of Canada cuts rates to offset trade headwinds.

Strategic Marker

1.42 on USD/CAD: a sustained move above this signals trade anxiety is dominating the oil benefit, often preceding broader risk off moves.

What could go wrong

Four reasons the market logic could fail

+

A coherent macro case is still only a case. Markets regularly ignore tidy narratives for longer than expected, or invalidate them quickly. Four failure paths stand out.

1

The situation de-escalates faster than the news cycle suggests

Geopolitical risk premia can build slowly and disappear quickly. Any credible sign of de-escalation, especially around shipping lanes or energy infrastructure, could reverse oil sharply and drain urgency from the rest of the thesis. This is precisely the scenario the TACO framework predicts.

2

Tariff posturing does not become tariff policy

The market may be reacting to opening positions rather than settled policy. If Washington and Beijing find a face-saving off-ramp, as they have in previous trade disputes, currency and equity moves that anticipated escalation could unwind just as fast as they built.

3

AI investment spending overrides the macro headwind

Technology capital expenditure has remained more resilient than expected for much of the past two years. If earnings season shows that AI infrastructure spending is still translating into real demand and returns, the growth narrative may reassert itself, particularly in the Nasdaq 100.

4

The squeeze never arrives: extended positioning holds for longer than expected

Stretched positioning does not automatically produce a violent reprice. Markets can stay under-owned for months if risk appetite remains weak and institutions are unwilling to rebuild exposure. The set-up can exist without the catalyst arriving in a way that forces the move.

Forward Calendar

What to watch and when

+

Three time horizons matter here. The first tests supply resilience. The second tests financial system health. The third tests whether any shift in market leadership is cyclical or structural.

Three horizon watchlist

Signals and catalysts across the next two months

Next Two Weeks

Chipmaker guidance and supply commentary

Major semiconductor earnings calls will offer an early read on whether supply bottlenecks are worsening and whether management teams are changing production assumptions. If supply commentary deteriorates, the inflation story gets another push and the case for higher for longer rates strengthens.

Next 30 Days

Bank earnings and loan demand

Major US banks will provide a useful check on whether capital spending related to AI infrastructure is still being financed. The most important signal may not be earnings per share. It may be commercial loan demand. If businesses are pulling back on borrowing, the growth cycle may be softening earlier than the market expects.

Next 60 Days

Enablers versus spenders

The more structural test is whether the market begins rewarding businesses that produce physical outputs: energy producers, hardware makers and defence contractors, while penalising software companies that still cannot prove a clear return on AI spending. A wider performance gap between those groups would suggest something deeper than a temporary rotation.

Jalan di depan

Konvergensi ketegangan geopolitik dan posisi ekstrem historis saat ini telah menciptakan lingkungan “mata air melingkar” yang unik untuk pasar global. Sementara TACO kerangka kerja menunjukkan pola eskalasi tajam diikuti oleh jeda strategis, ujian nyata bagi pedagang selama 60 hari ke depan adalah transisi dari volatilitas yang digerakkan oleh headline ke rotasi pasar struktural.

Apakah celah posisi ditutup melalui de-eskalasi lembut atau tekanan pendek yang keras, memiliki kerangka reaksi yang ditentukan dapat membantu pedagang menavigasi kebisingan.

Market Opportunity

Don't just watch the squeeze. Trade the framework.

As positioning gaps hit decade extremes, access advanced charting tools and real time execution on the six key markets defining this cycle.

Langkah terbaru dalam minyak telah menempatkan nama-nama energi kembali dalam fokus. Selama enam bulan terakhir, Exxon Mobil dan Baker Hughes telah mengungguli minyak mentah Brent secara normal, Chevron tetap konstruktif secara luas, SLB telah tertinggal dari komoditas dan konsensus broker Woodside telah lebih terukur.

Ketika minyak mentah bergerak, dampaknya jarang tetap terkendali pada komoditas itu sendiri. Harga minyak yang lebih tinggi dapat mempengaruhi ekspektasi inflasi, biaya pengiriman dan margin perusahaan di seluruh ekonomi global.

Apa yang ditunjukkan oleh langkah terbaru

Ada tiga cara besar perusahaan dapat memperoleh manfaat dari harga minyak yang lebih kencang:

Memproduksi minyak dan gas, dengan menjual komoditas dengan harga yang lebih tinggi

Menyediakan jasa dan peralatan kepada produsen

Mengangkut minyak ke seluruh dunia

Masing-masing nama di bawah ini mewakili salah satu jenis eksposur tersebut, dengan profil risiko yang berbeda ketika minyak mentah naik.

1. Exxon Mobil (NYSE: XOM)

Selama enam bulan terakhir, Exxon Mobil telah mengungguli minyak mentah Brent, dengan harga sahamnya naik hampir 35% dibandingkan dengan sekitar 30% untuk Brent. Pada 11 Maret 2026, keduanya diperdagangkan lebih dari 3% di bawah level tertinggi sepanjang masa, sementara Exxon tetap mendekati level tertinggi 52 minggu.

Exxon Mobil adalah salah satu perusahaan minyak terintegrasi terbesar di dunia, dengan eksposur yang mencakup eksplorasi, produksi, penyulingan, dan bahan kimia. Ketika harga minyak naik, bisnis hulu mungkin mendapat manfaat dari margin yang lebih luas, sementara skala dan diversifikasi dapat membantu melindungi bagian siklus yang lebih lemah.

Kinerja 6 bulan Exxon Mobil (XOM) vs Brent Crude

Minyak mentah Exxon Mobil dan Brent menormalkan kinerja selama enam bulan, pada 11 Maret 2026 pada saat penulisan | Sumber: Share Trader

Konsensus analis: Beli

Menurut data TradingView, sentimen analis terhadap Exxon secara luas positif. Dari 31 analis yang dilacak, 15 menilai saham Strong Buy atau Buy, 13 menilai itu Hold, 1 menilai Sell dan 2 menilai Strong Sell.

Pandangan positif itu terkait dengan kekuatan neraca Exxon dan produksi margin yang lebih tinggi. Analis paling optimis memproyeksikan target harga 1 tahun setinggi US $183,00. Target harga rata-rata adalah US$145,00, yang berada sekitar 3,6% di bawah harga perdagangan saat ini.

Peringkat analis Exxon Mobil dan target harga, per 11 Maret 2026 pada saat penulisan | Sumber: TradingView

2. Chevron (NYSE: CVX)

Chevron adalah perusahaan utama terintegrasi global lainnya yang telah mendapat manfaat dari pergerakan minyak mentah baru-baru ini yang lebih tinggi, dengan sahamnya diperdagangkan mendekati level tertinggi 52 minggu. Seperti Exxon, Chevron beroperasi di seluruh rantai nilai, termasuk produksi hulu, pemurnian dan pemasaran.

Akuisisi Chevron atas Hess yang telah selesai menambahkan Guyana dan aset hulu lainnya, yang dilihat oleh beberapa analis sebagai pendukung dari waktu ke waktu. Konon, dampak pendapatan tetap tunduk pada integrasi, pelaksanaan proyek dan risiko harga komoditas.

Kinerja Exxon Mobil vs Chevron, grafik 6 bulan

Chevron dan Exxon Mobil menormalkan kinerja selama enam bulan, pada 11 Maret 2026 pada saat penulisan | Sumber: Share Trader

Konsensus analis: Beli

Chevron dipandang mirip dengan Exxon, dengan sentimen broker tetap konstruktif secara luas. Agregat TradingView terbaru menunjukkan 30 analis yang mencakup saham selama tiga bulan terakhir, dengan 17 menilai itu Strong Buy atau Buy, 11 di Hold, 1 di Sell dan 1 di Strong Sell.

Analis telah menyoroti portofolio Chevron yang beragam dan potensi kontribusi dari Hess, meskipun volatilitas harga komoditas dan risiko eksekusi mungkin membuat beberapa orang lebih berhati-hati.

Peringkat analis Chevron dan target harga, per 11 Maret 2026 pada saat penulisan | Sumber: TradingView

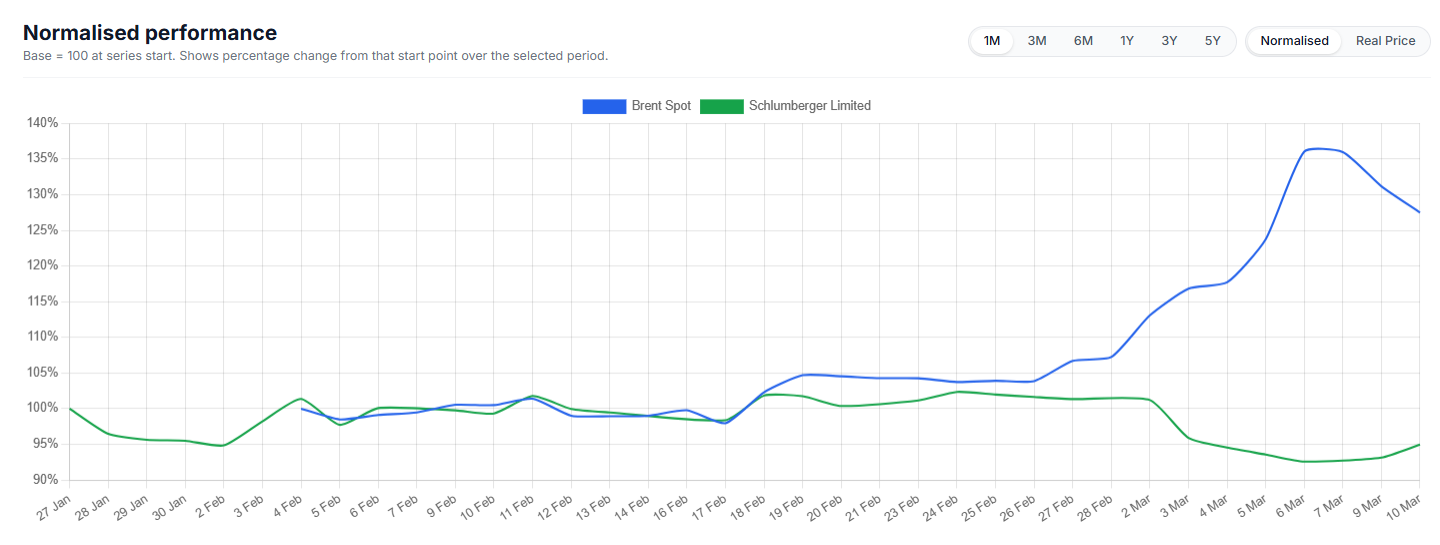

3. SLB (NYSE: SLB)

SLB, sebelumnya dikenal sebagai Schlumberger, adalah salah satu penyedia layanan ladang minyak dan teknologi terbesar di dunia. Ini memasok alat, peralatan, dan perangkat lunak yang membantu produsen menemukan, mengebor, dan menyelesaikan sumur dengan lebih efisien.

Selama enam bulan terakhir, SLB telah tertinggal dari minyak mentah Brent, dengan perdagangan harga saham dalam kisaran yang lebih tajam dan tetap di bawah puncaknya baru-baru ini. Itu menunjukkan latar belakang minyak yang lebih kuat belum sepenuhnya tercermin dalam harga saham.

Pola itu tidak biasa bagi perusahaan jasa ladang minyak, di mana keputusan pengeluaran pelanggan sering mengikuti pergerakan dalam komoditas yang mendasarinya daripada bergerak seiring dengan mereka. Setiap peringkat ulang di masa depan akan tergantung pada faktor-faktor termasuk pengeluaran modal produsen, waktu kontrak, harga layanan, aktivitas lepas pantai dan kondisi pasar yang lebih luas. Harga minyak yang lebih kuat seharusnya tidak diasumsikan secara otomatis diterjemahkan ke dalam harga saham SLB yang lebih kuat.

Minyak mentah SLB vs Brent, kinerja normal 6 bulan

Minyak mentah SLB dan Brent menormalkan kinerja selama enam bulan, per 11 Maret 2026 pada saat penulisan | Sumber: Share Trader

Konsensus: Beli

Menurut data TradingView, konsensus analis pihak ketiga tentang SLB adalah Beli. Dari 33 analis yang meliput saham, 27 menilai Strong Buy atau Buy, 4 menilai Hold dan 2 menilai Sell atau Strong Sell.

Itu menunjukkan sentimen broker yang konstruktif, meskipun kesenjangan antara harga minyak dan kinerja harga saham SLB baru-baru ini menunjukkan investor mungkin masih menginginkan bukti yang lebih jelas tentang peningkatan permintaan layanan dan penetapan harga sebelum saham sepenuhnya mencerminkan latar belakang komoditas yang lebih kuat.

Peringkat analis SLB dan target harga, per 11 Maret 2026 pada saat penulisan | Sumber: TradingView

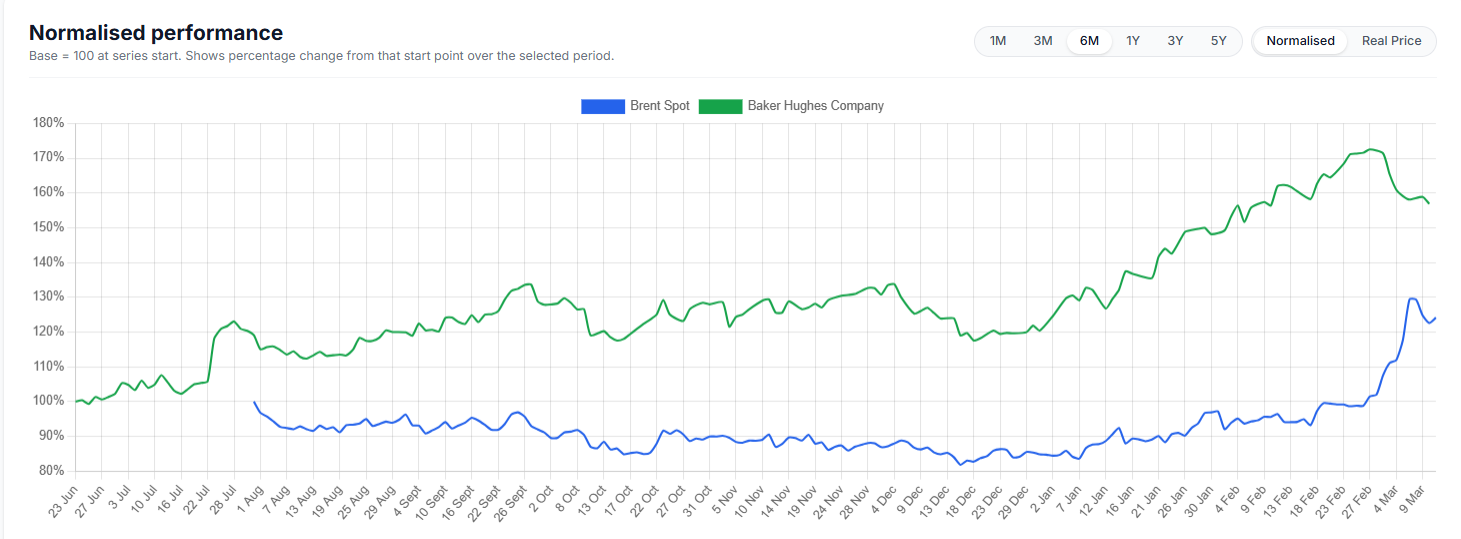

4. Baker Hughes (NASDAQ: BKR)

Baker Hughes adalah penyedia layanan dan peralatan ladang minyak utama lainnya, dengan eksposur tambahan ke segmen industri seperti LNG dan infrastruktur listrik. Bahkan ketika harga minyak tidak berada pada titik tertinggi yang ekstrim, kemajuan dalam teknologi pengeboran dan biaya impas yang lebih rendah telah membantu menjaga banyak permainan serpih menguntungkan, mendukung permintaan akan layanannya.

Perusahaan juga telah digambarkan sebagai posisi yang baik karena neraca dan eksposurnya terhadap aktivitas eksplorasi dan produksi yang sedang berlangsung. Dalam periode harga minyak yang lebih tinggi, atau bahkan stabil ke perusahaan, campuran layanan dan teknologi energi dapat menciptakan beberapa pendorong pendapatan.

Selama enam bulan terakhir, Baker Hughes secara material mengungguli minyak mentah Brent secara normal. Brent diperdagangkan dalam kisaran yang jauh lebih ketat untuk sebagian besar periode sebelum bergerak lebih tinggi akhir-akhir ini, sementara BKR naik lebih mantap dan mencapai keuntungan kumulatif yang jauh lebih kuat. Itu menunjukkan harga saham BKR diuntungkan tidak hanya dari latar belakang minyak, tetapi juga dari optimisme khusus perusahaan dan dukungan yang lebih luas untuk layanan ladang minyak dan nama teknologi energi.

Minyak mentah BKR vs Brent, kinerja normal 6 bulan

Baker Hughes dan minyak mentah Brent menormalkan kinerja selama enam bulan, pada 11 Maret 2026 pada saat penulisan | Sumber: Share Trader

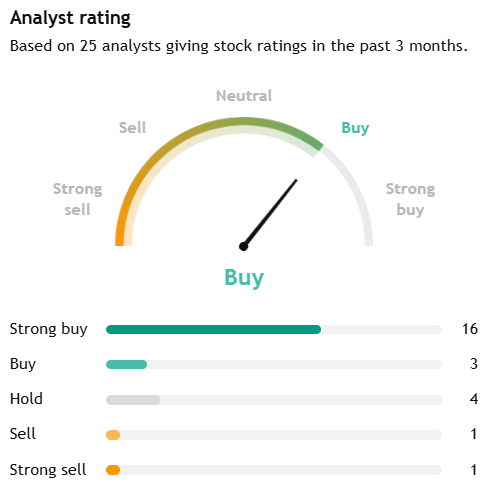

Konsensus analis: Beli

Menurut data TradingView, Baker Hughes dikategorikan sebagai Strong Buy. Berdasarkan 25 analis yang memberikan peringkat selama tiga bulan terakhir, 16 menilai saham Strong Buy, 3 menilai itu Beli, 4 menilai itu Hold, 1 menilai Sell dan 1 menilai Strong Sell.

Secara keseluruhan, sentimen broker terhadap Baker Hughes secara luas positif, dengan lebih dari tiga perempat analis penutupan menilai saham baik Strong Buy atau Buy, sementara sebagian besar sisanya berada di Hold. Pandangan analis yang mendukung itu tampaknya mencerminkan paparan BKR terhadap layanan ladang minyak tradisional dan pasar teknologi energi dan industri yang lebih luas, termasuk infrastruktur LNG.

Peringkat analis Baker Hughes dan target harga, per 11 Maret 2026 pada saat penulisan | Sumber: TradingView

5. Energi Woodside (ASX: WDS)

Woodside Energy memberikan daftar produsen yang berbasis di Australia dengan eksposur signifikan ke pasar LNG dan minyak. Pendapatannya terkait erat dengan harga komoditas yang direalisasikan, yang membuat saham sensitif terhadap perubahan harga minyak mentah dan gas, serta permintaan energi global yang lebih luas.

Dibandingkan dengan beberapa nama energi AS yang lebih besar, sentimen broker terhadap Woodside tampak lebih terukur. Investor menyeimbangkan eksposur LNG global perusahaan dan leverage terhadap harga energi yang lebih kuat terhadap harga realisasi baru-baru ini yang lebih lunak, risiko proyek dan eksekusi, serta tekanan regulasi dan dekarbonisasi jangka panjang.

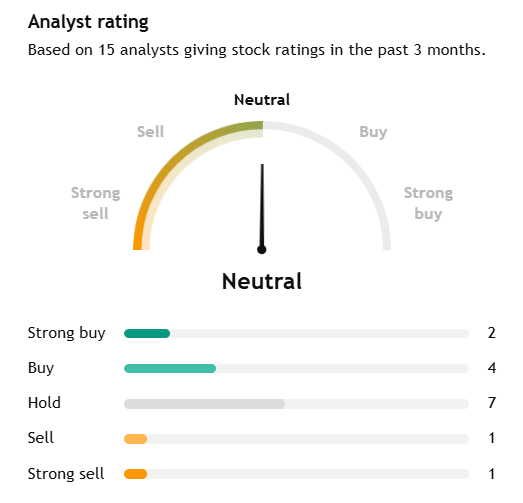

Konsensus analis: Tahan

Menurut data TradingView, Woodside dinilai Neutral/Hold. Dari 15 analis, 2 menilai itu Strong Buy, 4 menilai Beli, 7 menilai Hold, 1 menilai Sell dan 1 menilai Strong Sell.

Target harga rata-rata 12 bulan adalah A $29.20 versus harga saat ini sekitar A $30.28, menyiratkan penurunan sekitar 3.6%. Dibandingkan dengan nama energi AS yang lebih besar dalam daftar ini, itu menunjukkan pandangan broker yang lebih hati-hati.

Peringkat analis Woodside Energy dan target harga, per 11 Maret 2026 pada saat penulisan | Sumber: TradingView

6. Operator tanker minyak global

Perusahaan tanker minyak dapat memperoleh manfaat ketika harga minyak yang lebih kencang, perubahan kebijakan OPEC+ dan ketegangan geopolitik meningkatkan pengiriman jarak jauh dan mengganggu rute perdagangan biasa. Ketika volume minyak bergerak lebih jauh, permintaan 'tonne-mil' dapat mendukung tarif harian kapal tanker dan profitabilitas bahkan ketika pasar energi yang lebih luas tidak stabil.

Konsensus analis: N/A

Ini adalah kategori industri yang lebih luas daripada satu saham yang diperdagangkan secara publik, jadi tidak ada konsensus broker tunggal untuk dikutip. Pandangan analis perlu dinilai di tingkat perusahaan, seperti Frontline plc (FRO), Euronav (EURN) atau Scorpio Tankers (STNG).

Secara lebih luas, sektor ini bersifat siklus. Manfaat apa pun dari pasar pengiriman yang lebih ketat dapat berbalik jika rute menjadi normal, tarif pengiriman turun atau pasokan meningkat.

Risiko dan kendala

Harga minyak yang lebih tinggi tidak menghilangkan risiko untuk nama-nama ini.

Jika harga naik terlalu jauh, terlalu cepat, penghancuran permintaan dan respons kebijakan dapat membebani pendapatan di masa depan.

Keputusan politik dari OPEC+ atau produsen utama lainnya dapat membalikkan reli dengan meningkatkan pasokan.

Perusahaan jasa dan kapal tanker sangat siklis. Ketika siklus berubah, daya penetapan harga dapat memudar dengan cepat.

Masalah khusus perusahaan, termasuk pelaksanaan proyek, penetapan harga realisasi dan pengeluaran modal, masih penting.

Secara keseluruhan, nama-nama ini mungkin mendapat manfaat dari harga minyak yang lebih kuat, tetapi mereka juga membawa risiko spesifik sektor, geopolitik, dan tingkat perusahaan yang patut mendapat perhatian ketat.

Pengamatan pasar utama

Woodside menyediakan eksposur LNG dan minyak, meskipun sentimen broker saat ini lebih netral daripada untuk nama-nama AS yang lebih besar.

Operator kapal tanker mungkin mendapat manfaat ketika pasar angkutan mengencang, meskipun perdagangan itu tetap sangat siklis dan bergantung pada rute.

SLB dan Baker Hughes mungkin mendapat manfaat jika harga minyak yang lebih kuat diterjemahkan ke dalam lebih banyak kegiatan pengeboran dan penyelesaian, tetapi respons harga saham beragam.

Exxon Mobil dan Chevron menawarkan eksposur langsung ke margin hulu yang lebih kuat, didukung oleh diversifikasi operasi.

Referensi dalam artikel ini untuk Exxon Mobil, Chevron, SLB, Baker Hughes, Woodside, operator tanker, peringkat konsensus analis dan target harga disertakan hanya untuk komentar pasar umum dan bukan merupakan rekomendasi atau penawaran sehubungan dengan produk keuangan atau keamanan apa pun. Data pihak ketiga, termasuk peringkat konsensus dan harga target, dapat berubah tanpa pemberitahuan dan tidak boleh diandalkan secara terpisah. Eksposur energi dan pengiriman bersifat siklus dan dapat dipengaruhi secara material oleh volatilitas harga komoditas, penetapan harga yang direalisasikan, perubahan produksi, pelaksanaan proyek, gangguan geopolitik, kondisi pasar pengiriman, perkembangan peraturan, dan pergeseran sentimen investor. Setiap pandangan tentang calon penerima manfaat dari harga minyak yang lebih tinggi tunduk pada ketidakpastian yang signifikan.

Sebelum grafik mulai berbicara, wilayah melakukannya. Selama akhir pekan, Timur Tengah beralih dari tegang ke kinetik. Serangan gabungan AS dan Israel menghantam target di dalam Iran, dan beberapa outlet melaporkan Pemimpin Tertinggi Iran Ayatollah Ali Khamenei tewas. Fakta tunggal itu mengubah keseluruhan struktur kalimat pasar dan bukan hanya geopolitik, itu adalah premi risiko yang dihargai ulang secara real time, lintas energi, volatilitas, dan prospek pertumbuhan global.

Pasar tidak memperdagangkan tragedi, melainkan memperdagangkan ketidakpastian. Ketika ketidakpastian berada di atas arteri energi global, penemuan harga menurun.

Sekilas

Apa yang terjadi: Beberapa media besar melaporkan bahwa Pemimpin Tertinggi Iran Ayatollah Ali Khamenei tewas setelah serangan gabungan AS dan Israel di Iran, dengan media pemerintah Iran dikutip mengkonfirmasi kematiannya.

Apa yang mungkin difokuskan pasar sekarang: Penetapan harga ulang premia risiko geopolitik yang bergerak cepat, dipimpin oleh produk minyak mentah dan olahan, ditambah volatilitas lintas aset sebagai berita utama mendorong likuiditas, korelasi, dan rentang intraday.

Apa yang belum terjadi: Pasar mungkin menetapkan harga lebih dari premi risiko utama daripada gangguan pasokan fisik yang sepenuhnya terbukti dan berkelanjutan.

24 hingga 72 jam berikutnya: Fokus kemungkinan akan tetap pada sinyal eskalasi dan kendala tingkat kedua, termasuk dampak apa pun pada rute pelayaran Teluk dan kebijakan dan jalur diplomatik, termasuk dinamika Dewan Keamanan PBB.

Pengait Australia dan Asia: Gangguan penerbangan dan wilayah udara sudah meluas ke luar wilayah. Untuk pasar, sensitivitas yang menghadapi Asia dapat muncul melalui margin kilang dan biaya pengiriman dan asuransi, sementara AUD dapat berperilaku sebagai barometer risiko ketika selera risiko global tidak stabil.

Minyak adalah mekanisme transmisi

Minyak mentah Brent melonjak sebanyak 13% pada awal perdagangan pada Senin 2 Maret, menyentuh sekitar US $82 per barel dalam pelaporan, karena risiko Selat Hormuz bergerak dari teori ke langsung. Selat itu penting karena kira-kira seperlima pengiriman minyak dan gas global melewatinya dan ketika kapal tanker ragu, perusahaan asuransi memberi harga ulang, dan rute ditulis ulang, energi menjadi produk volatilitas.

Kasus dasar: gangguan parsional dan “premi risiko” yang lebih tinggi dalam minyak mentah, dengan perubahan intraday yang besar. Risiko naik: Perlambatan pengiriman berkelanjutan atau infrastruktur langsung, yang diperingatkan oleh beberapa analis dapat mendorong minyak mentah lebih tinggi secara material. Risiko penurunan: berita utama de-eskalasi, tanggapan pasokan darurat, atau perlindungan pengiriman yang lebih jelas yang menekan premi risiko.

VIX tidak bergerak dalam ruang hampa, dan lonjakan ketidakpastian ini sudah tumpah ke kelas aset lain dengan cara yang cukup 'buku teks'. Ketika volatilitas harga kembali, naluri pertama pasar adalah pelarian ke tempat yang aman, di samping perebutan komoditas yang paling terpapar konflik.

Senin melihat Asia dibuka dengan nada itu: Nikkei 225 Jepang dilaporkan turun sekitar 2.4%, dan ASX 200 Australia turun sebelum stabil. Pada saat yang sama, posisi defensif muncul di tempat aman klasik. Emas berjangka melemah lebih tinggi sekitar 3% selama akhir pekan, sementara mata uang perlindungan tradisional, yang dipimpin oleh franc Swiss, menarik arus masuk langsung terhadap euro dan dolar AS.

Risiko ekuitas, sebaliknya, mendapat pukulan. Indeks berjangka AS, termasuk Dow dan S&P 500, dibuka lebih rendah karena bursa bergerak ke harga dalam ancaman ganda konflik regional yang lebih luas dan hambatan inflasi yang dapat mengikuti lonjakan tajam dalam biaya energi.

Tempat berlindung yang aman melakukan apa yang mereka lakukan

Emas menguat seiring pasar mencapai asuransi. Pelaporan menunjukkan emas naik mendekati 3% pada sesi Senin yang sama ketika minyak melonjak. Perlu diperhatikan bagi pedagang Australia dan Asia: ketika minyak melonjak dan emas melonjak bersama, pasar sering memberi tahu Anda bahwa mereka khawatir tentang inflasi dan pertumbuhan. Itu adalah campuran yang berantakan untuk bank sentral, termasuk RBA, karena inflasi yang didorong oleh minyak dapat meningkat bahkan ketika permintaan melunak.

Apa artinya ini untuk manajemen risiko CFD

Fokus 1: memetakan kalender risiko acara

Di pasar yang digerakkan oleh headline, harga dapat bergerak lebih cepat daripada likuiditas. Risikonya bukan hanya salah; itu juga bisa menjadi risiko waktu dan eksekusi dalam kondisi yang tidak stabil.

Beberapa pedagang memantau perkembangan mana yang mungkin mengubah sentimen pasar (misalnya, pernyataan resmi atau pembaruan operasional terverifikasi). Jika Anda memilih untuk berdagang, mungkin ada baiknya memahami bagaimana kesenjangan harga dan volatilitas dapat memengaruhi posisi Anda, termasuk di sekitar sesi pembukaan dan pengumuman besar.

Pasar dapat mengalami gap atau bergerak cepat, dan eksekusi order (termasuk stop order, jika digunakan) mungkin tidak terjadi pada tingkat yang diharapkan, terutama dalam kondisi cepat atau likuiditas rendah. Fitur dan hasil tergantung pada syarat produk dan kondisi pasar.

Fokus 2: perhatikan jalur energi ke inflasi

Jika minyak mentah tetap tinggi, pasar mungkin melihat apakah ekspektasi inflasi bergeser. Jika itu terjadi, itu dapat mempengaruhi suku bunga, ekuitas dan FX dan meskipun hasilnya bergantung pada beberapa faktor dan dapat berubah dengan cepat.

Itu mungkin tercermin dalam:

Imbal hasil obligasi global, seiring dengan penyesuaian pasar suku bunga.

Sensitivitas penilaian ekuitas, terutama di area durasi panjang dan pertumbuhan berat.

FX bergerak, termasuk di seluruh dolar Australia, yen Jepang, dan beberapa mata uang terkait komoditas.

Pengumuman gencatan senjata 8 April dan diskusi paralel seputar gencatan senjata 45 hari belum menyelesaikan gangguan Selat Hormuz. Mereka, untuk saat ini, membatasi skenario terburuk, tetapi lalu lintas tanker tetap pada sebagian kecil dari tingkat normal dan permintaan Iran untuk biaya transit menandakan perubahan struktural, bukan yang sementara.

Apa yang dimulai sebagai konflik regional telah menjadi kejutan energi global, dan pertanyaan bagi pasar bukan lagi apakah Hormuz terganggu, tetapi seberapa permanen gangguan itu mengubah dasar harga untuk minyak.

Kuncinya yang menarik

Sekitar 20 juta barel per hari (bpd) minyak dan produk minyak bumi biasanya melewati Selat Hormuz antara Iran dan Oman, setara dengan sekitar seperlima dari konsumsi minyak global dan sekitar 30% dari perdagangan minyak laut global.

Ini adalah kejutan aliran, bukan masalah inventaris. Pasar minyak bergantung pada throughput berkelanjutan, bukan penyimpanan statis.

Jika gangguan berlanjut lebih dari beberapa minggu, Brent dapat bergeser dari lonjakan jangka pendek ke guncangan harga yang lebih luas, dengan risiko stagflasi.

Lalu lintas kapal tanker melalui selat turun dari sekitar 135 kapal per hari menjadi kurang dari 15 kapal pada puncak gangguan, pengurangan sekitar 85%, dengan lebih dari 150 kapal berlabuh, dialihkan, atau tertunda.

Gencatan senjata dua minggu diumumkan pada 8 April, dengan negosiasi gencatan senjata selama 45 hari sedang berlangsung. Iran secara terpisah telah mengisyaratkan permintaan biaya transit pada kapal-kapal yang menggunakan selat, yang, jika diformalkan, akan mewakili dasar geopolitik permanen pada biaya energi.

Pasar telah mulai berputar menjauh dari pertumbuhan dan eksposur teknologi terhadap nama energi dan pertahanan, mencerminkan pandangan bahwa kenaikan minyak menjadi biaya struktural daripada premi risiko sementara.

Institutional Grade Performance

Master the Markets with MetaTrader 5

Trade hundreds of instruments with superior speed and advanced technical analysis. Harness full EA functionality to execute your strategy.

Selat Hormuz menangani sekitar 20 juta barel per hari minyak dan produk minyak bumi, setara dengan sekitar 20% dari konsumsi minyak global dan sekitar 30% dari perdagangan minyak laut global. Dengan permintaan minyak global mendekati 104 juta barel per hari dan kapasitas cadangan terbatas, pasar sudah seimbang sebelum eskalasi terbaru.

Selat ini juga merupakan koridor penting untuk gas alam cair. Sekitar 290 juta meter kubik LNG transit setiap hari rata-rata pada tahun 2024, mewakili sekitar 20% dari perdagangan LNG global, dengan pasar Asia sebagai tujuan utama.

Badan Energi Internasional (IEA) telah menggambarkan Hormuz sebagai titik henti transit minyak yang paling penting di dunia, mencatat bahwa bahkan gangguan sebagian dapat memicu pergerakan harga yang terlalu besar. Minyak mentah Brent telah bergerak di atas US $100 per barel, mencerminkan keketatan fisik dan kenaikan premi risiko geopolitik.

Sumber: Administrasi Informasi Energi AS, tanggal 17 Juni 2025, menggunakan rata-rata harian 2024

Kapal tanker menganggur karena aliran lambat

Data pengiriman dan asuransi sekarang menunjukkan ketegangan secara real time. Lebih dari 85 kapal induk minyak mentah besar dilaporkan terdampar di Teluk Persia, sementara lebih dari 150 kapal telah berlabuh, dialihkan atau ditunda karena operator menilai kembali keselamatan dan asuransi. Itu akan meninggalkan sekitar 120 juta hingga 150 juta barel minyak mentah menganggur di laut.

Volume tersebut hanya mewakili enam hingga tujuh hari throughput Hormuz normal, atau sedikit lebih dari satu hari konsumsi minyak global.

Data pengiriman dan asuransi yang diperbarui sekarang mengkonfirmasi lebih dari 150 kapal telah berlabuh, dialihkan, atau tertunda, naik dari 85 yang awalnya dilaporkan. Cakupan konsumsi global 1,3 hari dari minyak mentah yang tidak digunakan tetap menjadi kendala yang mengikat: ini adalah kejutan aliran, bukan masalah penyimpanan, dan gencatan senjata belum diterjemahkan ke dalam throughput yang dipulihkan secara bermakna.

🌋 Trump, volatility and Hormuz.

As tariff shocks collide with a ten year extreme in oil positioning, the margin for error is zero. See the technical markers and safe haven pivots defining the current risk environment.

Pasar yang dibangun di atas aliran, bukan penyimpanan

Pasar minyak berfungsi pada pergerakan terus menerus. Kilang, pabrik petrokimia, dan rantai pasokan global dikalibrasi untuk pengiriman yang stabil di sepanjang jalur laut yang dapat diprediksi. Ketika aliran melalui titik henti yang membawa sekitar seperlima dari konsumsi minyak global dan sekitar 30% dari perdagangan minyak laut global terganggu, sistem dapat bergerak dari keseimbangan ke defisit dalam beberapa hari.

Kapasitas produksi cadangan, sebagian besar terkonsentrasi di OPEC, diperkirakan hanya 3 juta hingga 5 juta barel per hari. Itu jauh di bawah volume yang berisiko jika aliran Hormuz sangat terganggu.

GO Markets — Idle Tankers: Days of Cover

Oil market analysis

How long do idle tankers last?

135M idle barrels — days of cover against each demand benchmark

vs. Strait of Hormuz daily flow (20M bbl/day)

6.75 daysof Hormuz throughput covered

6.75 days

0

5

10

15

20

25

30 days

vs. Global oil consumption (104M bbl/day)

1.3 daysof world demand covered

1.3 days

0

5

10

15

20

25

30 days

vs. US Strategic Petroleum Reserve release (1M bbl/day)

135 daysof full SPR release pace covered

135 days — but SPR exists to replace this role

0

5

10

15

20

25

30 days

135M

idle barrels on tankers (midpoint of 120–150M range)

~33%

of daily Hormuz flow that is idle storage, not transit

<31 hrs

is all idle storage against global daily consumption

Indicative market trajectories based on disruption severity

Scenarios for the weeks ahead

1–2 WEEKS

Ceasefire catch-up

Markets face catch-up repricing. Brent could consolidate in the US$105–US$115 range as risk premia unwind. Brent may trade lower (US$95–US$110) if strategic stocks bridge the temporary shortfall.

2–4 WEEKS

Infrastructure blitz

Shifts to structural supply shock. Brent moving toward US$150–US$200 cannot be ruled out. This is the stagflation trigger where energy costs constrain central bank flexibility.

STRUCTURAL

Geopolitical floor

Iran's transit fee demand creates a permanent input cost. The pre-crisis price structure (US$60–US$70) may not return, embedded in insurance and freight rates.

Critical Threshold

US$120 remains the level at which energy inflation becomes a direct Federal Reserve policy problem.

Risiko inflasi dan limpahan makro

Dampak inflasi dari kejutan minyak biasanya datang dalam gelombang. Harga bahan bakar dan energi yang lebih tinggi dapat mengangkat inflasi utama dengan cepat karena biaya bensin, solar, dan listrik bergerak lebih tinggi.

Seiring waktu, biaya energi yang lebih tinggi dapat melewati pengiriman, makanan, manufaktur, dan layanan. Jika gangguan berlanjut, kombinasi peningkatan inflasi dan pertumbuhan yang lebih lambat dapat meningkatkan risiko lingkungan stagflasi dan membuat bank sentral menghadapi pertukaran yang sulit.

🛢️ Brent hits $100.

Exxon and SLB are leading the rotation out of tech. Get the price targets and technical support levels for the top 5 energy majors.

Tidak ada offset yang mudah, sistem dengan sedikit kelonggaran

Apa yang membuat episode saat ini sangat akut adalah kurangnya kelonggaran dalam sistem global.

Pasokan dan permintaan global mendekati 103 juta hingga 104 juta barel per hari meninggalkan sedikit bantalan cadangan ketika chokepoint penanganan hampir 20 juta barel per hari, atau sekitar seperlima dari konsumsi minyak global, terganggu. Diperkirakan kapasitas cadangan 3 juta hingga 5 juta barel per hari, sebagian besar di dalam OPEC, hanya akan mencakup sebagian kecil dari volume yang berisiko.

Rute alternatif, termasuk jaringan pipa yang melewati Hormuz dan mengalihkan rute pengiriman, hanya dapat mengimbangi sebagian arus yang hilang, dan biasanya dengan biaya yang lebih tinggi dan dengan waktu tunggu yang lebih lama.

Intinya

Sampai transit melalui Selat Hormuz dipulihkan dan dipandang aman secara kredibel, aliran minyak global kemungkinan akan tetap terganggu dan premi risiko meningkat. Bagi investor, pembuat kebijakan dan pembuat keputusan perusahaan, pertanyaan intinya adalah apakah minyak dapat bergerak ke tempat yang seharusnya, setiap hari, tanpa gangguan.

Market Opportunity

Don't just watch the squeeze. Trade the framework.

As positioning gaps hit decade extremes, access advanced charting tools and real time execution on the six key markets defining this cycle.

Sebuah berita utama tentang peradaban yang “sekarat malam ini” dibangun untuk membanjiri, tetapi sinyal yang lebih jelas mungkin adalah ketenangan di bawahnya, karena pasar mulai memperlakukan siklus eskalasi tajam ini diikuti oleh de-eskalasi mendadak sebagai pola, bukan kejutan.

Dalam lingkaran makro, pola itu memiliki label tumpul: TACO, atau “Trump Always Chickens Out”. Frasa dimuat, tetapi logikanya sederhana. Ancaman tekanan maksimum melanda, aset berisiko goyah, kemudian jeda, penundaan atau hasil yang lebih lembut muncul begitu biaya ekonomi mulai menggigit.

Itu tidak berarti risikonya kecil. Ini mungkin hanya berarti investor telah terbiasa dengan naskah di mana retorika berkobar, pasar menyerap guncangan, dan pengekangan muncul sebelum skenario terburuk sepenuhnya muncul.

Developing situation

|

Strait of Hormuz | Section 122 Tariffs

PublishedApril 2026

Brent CrudeAbove US$100

VIX31

In focus6 markets

Oil PositioningDecade-low longs

The Framework & MechanismIs the market the red line?

+

This is where the TACO idea starts to matter. Traders are not just watching the rhetoric. They are watching when it starts to hit markets, inflation and the wider economy.

Oil is at the centre of that risk. If disruption around the Strait of Hormuz starts to threaten global energy flows, the story quickly becomes macro. Higher oil can lift inflation expectations, pressure central banks and tighten financial conditions.

That is why a pause can look less like diplomacy and more like pressure relief. The real red line may be the point where the economic damage becomes too obvious to ignore.

Short Squeezed

Positioning adds another layer. Oil still looks under-owned, with futures positioning near decade-long bearish extremes. If a fresh shock lands, short-covering could drive prices higher much faster than fundamentals alone would suggest.

That is the short-squeeze risk. In the Commitment of Traders (COT) report, recent data suggests oil long exposure is relatively low by historical standards.

Humanitarian Reality

Whatever may be promised in political messaging, any sustained conflict in Iran would carry a heavy cost in displacement, infrastructure damage and wider regional stress. A relief rally in markets does not change that.

Global Isolation

Even if pauses are used to steady domestic market sentiment, allies and multilateral institutions may view bluff-and-retreat tactics as a credibility problem that creates longer-term diplomatic friction.

Positioning gap indicator

Divergence analysis between positioning and risk environment

APRIL 2026

Bars show GO Markets’ internal estimate of the divergence between current futures positioning and levels seen in comparable historical shock environments.

Brent crudeExtreme

Gold (XAU/USD)Very high

Nasdaq 100High

USD/CNHHigh

US 10 yr yieldMedium

USD/CADMedium

Extreme decade scale positioning extreme

High significant divergence

Medium moderate divergence

Methodology note

The Positioning Gap Indicator is based on GO Markets’ internal analysis and is intended as a high-level, illustrative framework only. It uses a combination of market positioning data, historical comparisons and discretionary assumptions about how similar energy and trade shocks have affected markets in the past. The ‘Extreme’, ‘Very High’, ‘High’ and ‘Medium’ labels are relative internal classifications, not objective market standards, and should not be relied on as predictions, forecasts or a guarantee of future outcomes.

The Six Markets

The six markets that matter most

Each of these six markets is exposed to the current situation through a different mechanism. Understanding the mechanism, not just the price, matters. It helps explain whether a move is a headline reaction or the start of something broader. Tap any card to expand the full analysis.

01

BRENT

Brent crude oil

ENERGYDIRECT CHANNELSQUEEZE RISK: EXTREME

+

The Clear Transmission Channel

Brent is the international benchmark for crude and the most direct transmission mechanism in this geopolitical thesis. Any disruption to physical flows, particularly through the Strait of Hormuz, forces an immediate tightening of global energy supply.

The Positioning Backdrop

Futures positioning currently sits at a ten year bearish extreme. Leveraged funds have cut long exposure heavily. In the event of a physical supply shock, this imbalance creates the potential for a violent short covering squeeze.

● Bull Case

Hormuz disruption extends beyond four weeks. Extended disruption could lift Brent sharply if supply flows are impaired for longer.

● Bear Case

Diplomatic intervention reopens the strait quickly. Strategic petroleum reserve (SPR) releases and increased spare capacity cap any price rally.

Strategic Marker

US$120: the point at which energy inflation becomes a direct Federal Reserve policy problem, rather than just a market narrative.

02

XAU/USD

Gold

SAFE HAVENUNDER-OWNEDSQUEEZE RISK: VERY HIGH

+

The Counter-Intuitive Setup

Despite a clear geopolitical risk profile, leveraged funds have been reducing bullish gold exposure. This leaves the market under-owned at the exact moment the fundamental case for safe haven assets is strengthening.

The Inflation Variable

The critical factor for Gold is whether energy-driven inflation limits the Fed's room to maneuver. If policy flexibility weakens, Gold could catch up quickly as a hedge against stagflation.

● Bull Case

Real yields fall as energy inflation outpaces rate hikes. Under-owned positioning amplifies the catch up move as institutional funds rebuild exposure.

● Bear Case

Geopolitical tensions ease rapidly. The Fed remains credibly focused on inflation, keeping real yields positive and supporting the USD over Gold.

Strategic Marker

One level to monitor is prior resistance, alongside any change in COT positioning.

03

US100/NAS100

Nasdaq 100

TECHNOLOGYDUAL PRESSURERATE AND SUPPLY RISK

+

Why it is a complicated position

The Nasdaq faces immediate pressure from two fronts: Stickier energy-driven inflation forces rates higher for longer, compressing multiples, while trade tensions unsettle the supply chains beneath major tech names.

Why the 10 year yield matters here

When the 10 year Treasury yield holds above 4.5%, the future value of technology earnings must be discounted at a higher rate. AI linked earnings momentum must overpower this valuation headwind.

● Bull Case

Earnings season delivers proof of AI investment generating real revenue. Index components successfully insulate supply chains, and AI capex momentum overrides the macro headwind.

● Bear Case

Energy inflation keeps yields above 4.5%. Multiple compression in high valuation names triggers a broader index decline amid disappointments in AI monetization.

Strategic Marker

S&P 500 at 6,498: a widely watched Fibonacci cluster. A sustained move below this threshold highlights a historically challenging framework for growth equities.

04

USD/CNH

US dollar/offshore Chinese yuan

FXBEIJING READPOLICY PROXY

+

What it tells you

USD/CNH is the cleanest real time read on how Beijing is responding to tariff pressure. A sharp rise suggests China is allowing currency weakness to absorb the costs of trade friction.

Why it matters beyond China

A move in USD/CNH doesn't stay contained. It spills into Asian equities, commodity demand, and broader risk appetite. Deliberate depreciation signals a shift in the global trade environment.

● USD Bull / Yuan Bear

Beijing allows yuan weakness as a deliberate countermeasure. Capital outflows accelerate, and USD safe haven demand reinforces the move.

● Yuan Recovery

Trade negotiations begin and a face saving off ramp is found. PBOC intervention defends the yuan, and the dollar's safe haven premium fades.

Strategic Marker

7.30 on USD/CNH: a sustained move above this has historically been associated with broader risk off moves in Asian markets.

05

US10Y/TNOTE

US 10 year Treasury yield

RATESMACRO PLUMBINGSHAPES EVERYTHING ELSE

+

Why it sits under everything

The 10 year yield shapes mortgage costs, corporate borrowing, and the valuation framework for risk assets globally. When it rises, borrowing becomes more expensive across the entire system.

The Independent Movement Risk

If oil forces the Fed to delay cuts, the 10 year yield could rise regardless of Fed communication. It can tighten financial conditions even before a formal policy shift occurs.

● Rates Fall Case

Oil shock proves transient. Fed maintains guidance and 10 year yields pull back toward 4.0%, relieving pressure on equities and providing support for bonds.

● Rates Rise Case

Sustained oil above US$100 pushes inflation higher. Fed pauses rate cut language and the 10 year yield breaks above 4.5%, compressing equity multiples.

Strategic Marker

4.5% on the 10 year yield: a sustained break above this while oil remains above US$100 is a historically challenging combination for equities.

06

USD/CAD

US dollar/offshore Canadian dollar

FXOIL-LINKEDLEAD INDICATOR

+

The Double Exposure

USD/CAD is a lead indicator because Canada sits at the intersection of energy and trade. It benefits from higher oil revenue but is highly sensitive to US economic and trade conditions.

When the Forces Collide

When oil rises, the CAD often strengthens; when trade stress rises, it weakens. In the current environment, these forces are colliding rather than canceling each other out.

● CAD Strengthens

Oil sustained above US$100 boosts export revenue while trade tensions stay short of Canada specific tariffs. Bank of Canada holds rates steady.

● CAD Weakens

Safe haven USD demand outweighs the oil benefit. Bank of Canada cuts rates to offset trade headwinds.

Strategic Marker

1.42 on USD/CAD: a sustained move above this signals trade anxiety is dominating the oil benefit, often preceding broader risk off moves.

What could go wrong

Four reasons the market logic could fail

+

A coherent macro case is still only a case. Markets regularly ignore tidy narratives for longer than expected, or invalidate them quickly. Four failure paths stand out.

1

The situation de-escalates faster than the news cycle suggests

Geopolitical risk premia can build slowly and disappear quickly. Any credible sign of de-escalation, especially around shipping lanes or energy infrastructure, could reverse oil sharply and drain urgency from the rest of the thesis. This is precisely the scenario the TACO framework predicts.

2

Tariff posturing does not become tariff policy

The market may be reacting to opening positions rather than settled policy. If Washington and Beijing find a face-saving off-ramp, as they have in previous trade disputes, currency and equity moves that anticipated escalation could unwind just as fast as they built.

3

AI investment spending overrides the macro headwind

Technology capital expenditure has remained more resilient than expected for much of the past two years. If earnings season shows that AI infrastructure spending is still translating into real demand and returns, the growth narrative may reassert itself, particularly in the Nasdaq 100.

4

The squeeze never arrives: extended positioning holds for longer than expected

Stretched positioning does not automatically produce a violent reprice. Markets can stay under-owned for months if risk appetite remains weak and institutions are unwilling to rebuild exposure. The set-up can exist without the catalyst arriving in a way that forces the move.

Forward Calendar

What to watch and when

+

Three time horizons matter here. The first tests supply resilience. The second tests financial system health. The third tests whether any shift in market leadership is cyclical or structural.

Three horizon watchlist

Signals and catalysts across the next two months

Next Two Weeks

Chipmaker guidance and supply commentary

Major semiconductor earnings calls will offer an early read on whether supply bottlenecks are worsening and whether management teams are changing production assumptions. If supply commentary deteriorates, the inflation story gets another push and the case for higher for longer rates strengthens.

Next 30 Days

Bank earnings and loan demand

Major US banks will provide a useful check on whether capital spending related to AI infrastructure is still being financed. The most important signal may not be earnings per share. It may be commercial loan demand. If businesses are pulling back on borrowing, the growth cycle may be softening earlier than the market expects.

Next 60 Days

Enablers versus spenders

The more structural test is whether the market begins rewarding businesses that produce physical outputs: energy producers, hardware makers and defence contractors, while penalising software companies that still cannot prove a clear return on AI spending. A wider performance gap between those groups would suggest something deeper than a temporary rotation.

Jalan di depan

Konvergensi ketegangan geopolitik dan posisi ekstrem historis saat ini telah menciptakan lingkungan “mata air melingkar” yang unik untuk pasar global. Sementara TACO kerangka kerja menunjukkan pola eskalasi tajam diikuti oleh jeda strategis, ujian nyata bagi pedagang selama 60 hari ke depan adalah transisi dari volatilitas yang digerakkan oleh headline ke rotasi pasar struktural.

Apakah celah posisi ditutup melalui de-eskalasi lembut atau tekanan pendek yang keras, memiliki kerangka reaksi yang ditentukan dapat membantu pedagang menavigasi kebisingan.

Market Opportunity

Don't just watch the squeeze. Trade the framework.

As positioning gaps hit decade extremes, access advanced charting tools and real time execution on the six key markets defining this cycle.

Jadi inilah masalahnya: musim pendapatan AS April tiba di pasar yang masih terasa sama sekali tidak normal. Seperti yang dijelaskan GO Markets di Buku pedoman pendapatan AS global: Panduan penting untuk pedagang, periode pelaporan ini mendarat setelah perubahan nyata dalam apa yang dipedulikan pasar. Ini bukan lagi hanya tentang mengejar pertumbuhan dengan biaya berapa pun. Ini tentang apa yang dikatakan angka-angka di bawah permukaan.

Dan pada tahun 2026, sinyal-sinyal itu bertabrakan dengan latar belakang gesekan tinggi:

Konflik geopolitik: Ketegangan yang sedang berlangsung di Timur Tengah

Kejutan pasokan minyak: Minyak mentah Brent di atas US $100

The Fed: Bank Sentral Masih Terkena Inflasi

Pivot daya tahan

Ya, AI masih menjadi cerita utama pasar tetapi masih mesin mencolok yang mendapatkan sebagian besar perhatian. Tapi di bawahnya, ada langkah yang lebih tenang menuju perusahaan yang terlihat dibangun untuk bertahan lebih baik ketika kondisinya semakin sulit.

Ketika tarif tidak pasti dan pasar energi berada di bawah tekanan, nama-nama seperti JPMorgan Chase dan kontraktor pertahanan utama mulai membawa lebih banyak bobot. Mereka tidak menggantikan narasi AI, melainkan, mereka menjadi bagian dari cara pedagang membaca selera risiko, daya tahan pendapatan dan, pada akhirnya, di mana pasar mencari sesuatu yang lebih solid untuk dipertahankan.

!

Important: Reporting schedules can change without notice. Reporting dates and release times are from company investor relations calendars where marked Confirmed; otherwise they are GO Markets estimates. Consensus EPS, revenue and analyst-range data are from third-party market consensus sources, as of 7 April 2026 (AEDT). Company guidance, backlog and operating metrics are from the latest company filings or results presentations unless stated otherwise. Figures and schedules may change without notice.

$JPM| Q1 2026 REPORTING PERIOD

JPMorgan Chase & Co.

NYSE | Financial Services | 14 Apr 2026

Confirmed

Global Release Countdown (BMO)

00:00:00:00

Consensus EPS

US$5.42

Consensus Revenue

US$47.88bn

AU/ASIA14 Apr | 8:45 pm

US/LATAM14 Apr | 6:45 am

Market Intelligence: $JPM

Analysis: JPM price drivers and scenarios

NII guidance

~US$103 billion

Full year | US$95 billionn ex:markets

ROTCE target

17%

Possible return on tangible common equity

Analyst range

US$5.02-5.70

Low to high estimate spread

AVG

LOW US$5.02AVG US$5.39HIGH US$5.70

The analyst spread of US$0.68 signals genuine disagreement about how the rate environment is flowing through to margins. A result above consensus but below the high end estimate may produce a muted reaction. A result above US$5.70 may shift the discussion.

Key swing factors for the result

Net interest income (NII)

The clearest macro lever. It reflects the gap between lending rates and deposit costs.

Guidance: US$103 billion for the full year

Return on tangible common equity (ROTCE)

A scale check. It indicates whether JPM is converting scale into efficiency. 17% is the benchmark.

Target: 17% ROTCE

Trading and investment banking

Strong Q1 growth was expected in fees and markets revenue. These lines can offset softness in lending, and stronger-than-expected performance here may shift the narrative away from rate sensitivity.

Watch: investment banking (IB) fees versus the prior quarter

Expense discipline

A bank can beat the EPS estimate and still sell off if expense growth is running too hot. Pairing the EPS result with the expense trajectory gives a fuller read on whether the beat is durable.

Watch: Expense outlook commentary

Trade Execution: $JPM

Earnings reaction framework: Q1 2026

Bull case

EPS above US$5.70, NII on track | ROTCE at or above 17%

The result comes in above the top of the analyst range. NII guidance holds or is revised higher. IB fees and markets revenue show strong Q1 growth. Expense commentary is constructive.

Possible reaction: momentum and repositioning

Base case

EPS between US$5.39 and US$5.70, NII in line | ROTCE near target

The result beats consensus but stays within the expected range. NII tracks guidance. The tone of the conference call may matter more than the headline number. The first move may fade if guidance is unchanged.

Possible reaction: muted or mixed initial response

Bear case

EPS below US$5.39 | NII misses | Expense growth surprises

The result comes in at or below the consensus midpoint. NII guidance is cut or qualified. Expense growth comes in above market expectations. IB or markets revenue disappoints.

Possible reaction: earnings multiple repricing

Reaction trigger to watch: The market response in the first 30 minutes after the result may indicate which scenario traders are leaning towards. A move above the prior session high on volume may support the bull case. A fade back into the range after an initial pop may point to the base case. A break below the prior session low on volume may suggest the bear case is gaining traction.

Sentiment Analysis · JPMorgan Chase

Interactive scenario analysis: $JPM

Select earnings outcome

Growth momentum

AI-linked offset, beat supported by NII and ROTCE

Stronger-than-expected demand for AI-related industrial lending may offset softer mortgage activity. Management maintains guidance as NII remains resilient in higher-for-longer conditions. IB fees and markets revenue may provide additional support. ROTCE at or above 17% would suggest the bank is converting scale into earnings efficiently.

EPS Outcome

Above US$5.70

NII Signal

On track

ROTCE

At or above 17%

Likely Reaction

Momentum may build

Sources & Data Methodology

Sources: Reporting dates and release times are from company investor relations calendars where marked Confirmed; otherwise they are GO Markets estimates. Consensus EPS, revenue and analyst-range data are sourced from Bloomberg and Earnings Whispers, as at 7 April 2026 (AEDT). Company guidance, backlog and operating metrics are sourced from the latest company filings, results presentations or investor relations materials unless stated otherwise. Any scenario analysis reflects GO Markets analysis. Figures and schedules may change without notice.

From credit to defence

If JPMorgan gives the market an early read on the consumer, credit quality and business activity, the defence names may be telling a different story. This is the point where the focus may start to shift from the credit cycle to government-backed demand.

In a market still shaped by geopolitical risk, that matters. Long-dated programs can help support revenue visibility, even when the broader outlook looks less certain. That is one reason the sector remains on the watchlist.

$LMT| Q1 2026 REPORTING PERIOD

Lockheed Martin Corp.

NYSE | Aerospace | Defense | 22 Apr 2026

Estimated

Global Release Countdown (BMO)

00:00:00:00

Consensus EPS

US$6.50

Consensus Revenue

US$16.32bn

AU | ASIA22 Apr | 9:20 pm

US | LATAM22 Apr | 7:20 am

Market Intelligence: $LMT

Analysis: LMT price drivers and scenarios

Order backlog

US$194 billionn

Record visibility

Book-to-bill

1.2x

Orders outpacing sales

Analyst range

US$6.90-7.10

Low to high estimate spread

AVG

LOW ~US$6.90AVG ~US$6.94HIGH US$7.10+

The consensus sits near the lower end of the analyst range. That positioning may leave room for upside if backlog growth and F-35 delivery timelines support execution. A print near the high end, above US$7.10, may extend the move, although the reaction would still depend on guidance and margins.

Key swing factors for the result

Backlog visibility

Primary evidence of demand. Book-to-bill above 1.2x would support full-year guidance and the production ramp.

Backlog: US$194 billion record

Free cash flow (FCF)

Defence stocks are often assessed on cash conversion. The market may look for confirmation of the US$6.5 billion floor.

Guide: US$6.5 billion - $6.8 billion

Missile segment growth

PrSM and THAAD deliveries remain key watchpoints. Strong space margins may help offset softness in aeronautics.

Watch: Fire Control margins

Margin pressure

Pension charges and production inflation remain risks. An earnings beat may fade if operating margins contract.

The result clears the upper half of the analyst range. Management reaffirms or raises the full-year FCF outlook. Strong Missiles and Fire Control (MFC) margins help offset any aeronautics supply chain lag.

Possible reaction: momentum may build and positioning may improve

Base case

EPS between US$6.30 and US$6.70 | Backlog steady at about US$194 billion

The result aligns with the US$6.38 consensus. F-35 delivery pace remains on track but offers no meaningful upside surprise. The market may wait for more specific segment guidance on the conference call.

Possible reaction: muted or mixed initial response

The result falls towards the bottom of the analyst spread. Management cites further software delays or program losses. The FCF trajectory narrows towards the lower end of previous expectations.

Possible reaction: the share price may come under pressure

Reaction trigger to watch: The market response in the first 30 minutes after the result may indicate which scenario traders are leaning towards. A move above the prior session high on volume may support the bull case. A fade back into the range after an initial pop may point to the base case. A break below the prior session low on volume may suggest the bear case is gaining traction.

Sentiment Analysis · Lockheed Martin

Interactive scenario analysis: $LMT

Select earnings outcome

Backlog confirmed

Backlog and FCF confirmation may support continuation

EPS clears the top of the analyst range. Backlog holds at or above US$194 billion and book-to-bill stays above 1.2, which would suggest orders are replenishing faster than revenue is being recognised. FCF guidance holds within the stated range.

EPS outcome

Above US$7.00

Backlog signal

Above US$194 billion

FCF guide

Holds or improves

Likely reaction

Continuation may follow

Sources & Data Methodology

Sources: Reporting dates and release times are from company investor relations calendars where marked Confirmed; otherwise they are GO Markets estimates. Consensus EPS, revenue and analyst-range data are sourced from Bloomberg and Earnings Whispers, as at 7 April 2026 (AEDT). Company guidance, backlog and operating metrics are sourced from the latest company filings, results presentations or investor relations materials unless stated otherwise. Any scenario analysis reflects GO Markets analysis. Figures and schedules may change without notice.

Not all defence names are the same

Lockheed Martin and Northrop Grumman may sit in the same defence bucket, but the market does not always read them the same way. Lockheed is more closely tied to the F-35 and current air combat demand. Northrop is more closely linked to next-generation programs such as the B-21 Raider and Sentinel.

That gives this section its contrast. One is often read through the lens of current defence demand. The other is more closely tied to longer-cycle strategic modernisation.

$NOC| Q1 2026 REPORTING PERIOD

Northrop Grumman Corp.

NYSE | Defense | Space Systems | 23 Apr 2026

Estimated

Global Release Countdown (BMO)

00:00:00:00

Consensus EPS

US$6.12

Consensus Revenue

US$10.24 bn

AU | ASIA23 Apr | 10:30 pm

US | LATAM23 Apr | 8:30 am

Market Intelligence: $NOC

Analysis: NOC price drivers and scenarios

Consensus EPS

US$6.96

Quarterly analyst average

Order Backlog

US$95.7 billion

Record revenue visibility

FY 2026 EPS guide

US$27.40-US$27.90

Full-year 2026 outlook

AVG

LOW ~US$6.90AVG ~US$6.96HIGH US$7.20+

The consensus sits near the lower end of the analyst range. That offers a quick visual for whether the result is merely in line or strong enough to ease the guidance concerns that weighed on the stock after its last update. A result above US$7.20 may shift the conversation more materially.

Key swing factors for the result

Book-to-bill ratio

Currently at 1.10, suggesting orders are still running ahead of revenue recognition. This remains an important signal for multi-year growth visibility in defence.

Watch: 1.10 target

Guidance reset risk

Management’s guidance previously came in below market expectations. The market may be sensitive to any further softening in the 2026 outlook.

Watch: guidance commentary

Program concentration

The B-21 Raider and Sentinel carry outsized execution sensitivity. Updates on production ramp and funding may be the clearest drivers of sentiment for the stock.

Watch: B-21 and Sentinel updates

Capacity investment

Higher capital expenditure (capex) supports the industrial base over the longer term, but it may pressure near-term margins. Watch for signs that current investment is weighing on earnings power.

The result comes in above the cited threshold. Management says B-21 Raider production is ahead of schedule, with improving margins. Sentinel program restructuring costs remain below baseline expectations. International awards lift the book-to-bill ratio above 1.15.

Possible reaction: momentum may improve

Base case

EPS between US$6.00 and US$6.20, backlog steady at about US$95.7 billion

The result is broadly in line with the cited range. FCF targets for 2026 are reaffirmed but not expanded. Market focus shifts to organic sales growth metrics and segment operating margins. The initial reaction may depend on the timing of B-21 milestone payments.

The result lands near the low end of the analyst spread. Management flags higher infrastructure costs for Sentinel or delays in restricted space segment awards. Margin pressure in Aeronautics persists, and the 2026 revenue guide narrows towards the US$43.5 billion floor.

Possible reaction: shares may weaken

Reaction trigger to watch: The market response in the first 30 minutes after the result may indicate which scenario traders are leaning towards. A move above the prior session high on volume may support the bull case. A fade back into the range after an initial pop may point to the base case. A break below the prior session low on volume may suggest the bear case is gaining traction.

Sentiment Analysis · Northrop Grumman

Interactive scenario analysis: $NOC

Select earnings outcome

Stealth momentum

B-21 momentum, stronger execution and FCF support

EPS clears US$6.15. Management confirms a production capacity agreement for the B-21 Raider. Sentinel restructuring reaches Milestone B on schedule. Record backlog visibility and higher FCF guidance towards US$3.5 billion may support broader repositioning.

EPS outcome

Above US$6.15

B-21 Signal

Acceleration

FCF guide

$3.5 billionn range

Likely reaction

Momentum rally

Sources & Data Methodology

Sources: Reporting dates and release times are from company investor relations calendars where marked Confirmed; otherwise they are GO Markets estimates. Consensus EPS, revenue and analyst-range data are sourced from Bloomberg and Earnings Whispers, as at 7 April 2026 (AEDT). Company guidance, backlog and operating metrics are sourced from the latest company filings, results presentations or investor relations materials unless stated otherwise. Any scenario analysis reflects GO Markets analysis. Figures and schedules may change without notice.

Bottom line