Coal and Gas prices have surged and joined gold and oil as demand surges due to the supply shortages stemming from the Russia and Ukraine conflict. The global indices were up overall as the market still remains unsure of how to react to the unfolding crisis. In Europe, the FTSE provided strength with a 1.36% gain and the DAX provided a small bounce rising 0.69%.

In America the Dow Jones and the NASDAQ both saw decent rises, moving 1.79% and 1.62% respectively. The US markets responded positively after Jerome Powell testified that the Federal Reserve still intends to increase interest rates later this month by 25 basis points. Mr.

Powell did, however, allow for some flexibility in the face of the increased conflict. The biggest mover was coal which shot up almost 33% to $400 on the back of the energy crisis. It has led to many countries attempting to scavenge for coal reserves.

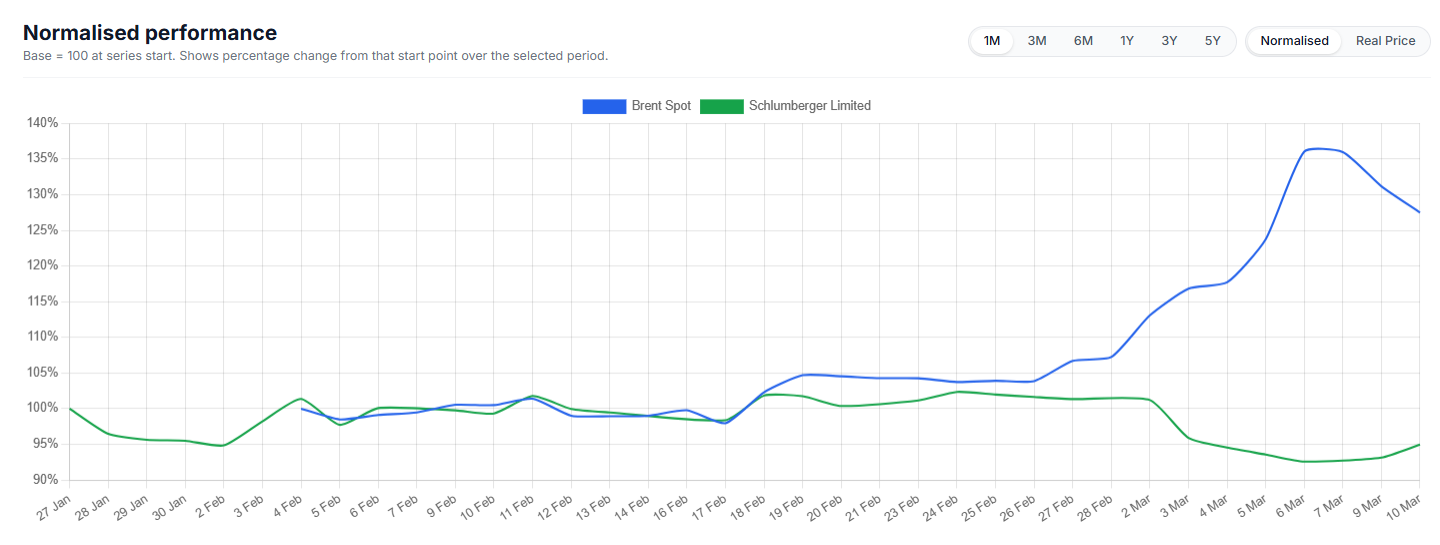

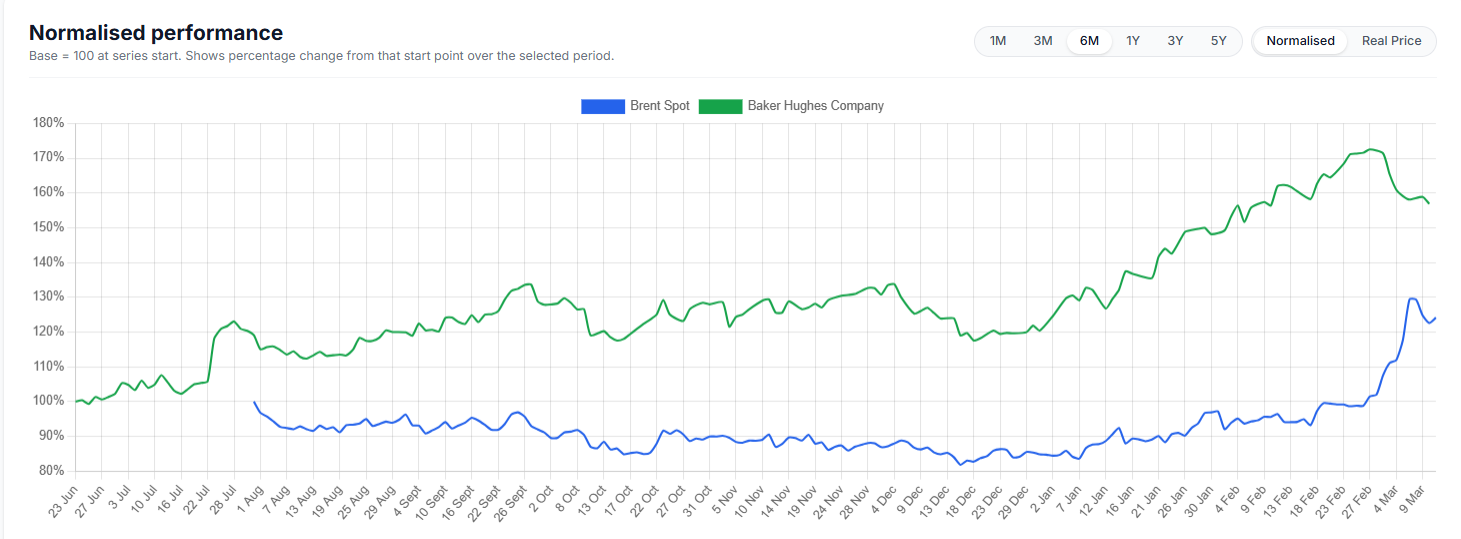

Germany is poised to create coal power reserves and Italy announced it may reopen some of its previously shut coal plants. The Aussie dollar has benefited from this and other rises in commodity prices with AUDUSD touching on 0.73c overnight. Oil prices reached as high as $114.00 and touched the 8 year high before settling in at $111.

This is after OPEC decided overnight to hold production level at the current level leaving the potential shortfall in demand unaccounted for, claiming that that demand for oil is being driven by geopolitics and not fundamentals. The price of wheat and aluminium also hit 14-year highs overnight and Gold continues to remain steady at $1,927 per ounce. Bitcoin saw a slight slump and is down 1.47% although is still very much moving upward due to the momentum from Russian investors.

The Ruble saw some strength as it saw upward of 5% gains against many other currency pairs. The US dollar continues to be strong on the back of the Federal reserve and from the risk aversion seen in the market at the moment.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. 免责声明:文章来自 GO Markets 分析师和参与者,基于他们的独立分析或个人经验。表达的观点、意见或交易风格仅代表作者个人,不代表 GO Markets 立场。建议,(如有),具有“普遍”性,并非基于您的个人目标、财务状况或需求。在根据建议采取行动之前,请考虑该建议(如有)对您的目标、财务状况和需求的适用程度。如果建议与购买特定金融产品有关,您应该在做出任何决定之前了解并考虑该产品的产品披露声明 (PDS) 和金融服务指南 (FSG)。

.jpeg)