Never has the oil been trickier than it is right now. The influences on the price are complex, varied and time dependent. It’s even trickier when you look at it from the trade of commodities versus equities.

Here are the key things that are catching our attention with oil trading in spot, forwards and equities. Spot vs. Anticipatory Market While WTI and Brent prices are influenced by current ('spot') market conditions, they are not solely determined by them.

There is a level of anticipation of supply, and these are priced through mechanisms like storage and forward curves. This allows the market to shift supply into the future or pull it forward as required. Right now however, demand and supply are so out of traditional cycles, pull forwarded supply is being re-stocked and future supply cut to offset the current scenario.

This might explain why forward curves are inverting – these curves are crucial in regulating the anticipatory nature of oil prices. Forward curves represent the market's expectation of future prices and influence current trading behaviours. Clearly even with supply cuts.

The market expects price to fall further if the forward curves are to be believed. Investment Time Horizons Do not forget the fundamental market pricing in equities. Share prices reflect prospective multi-year earnings growth.

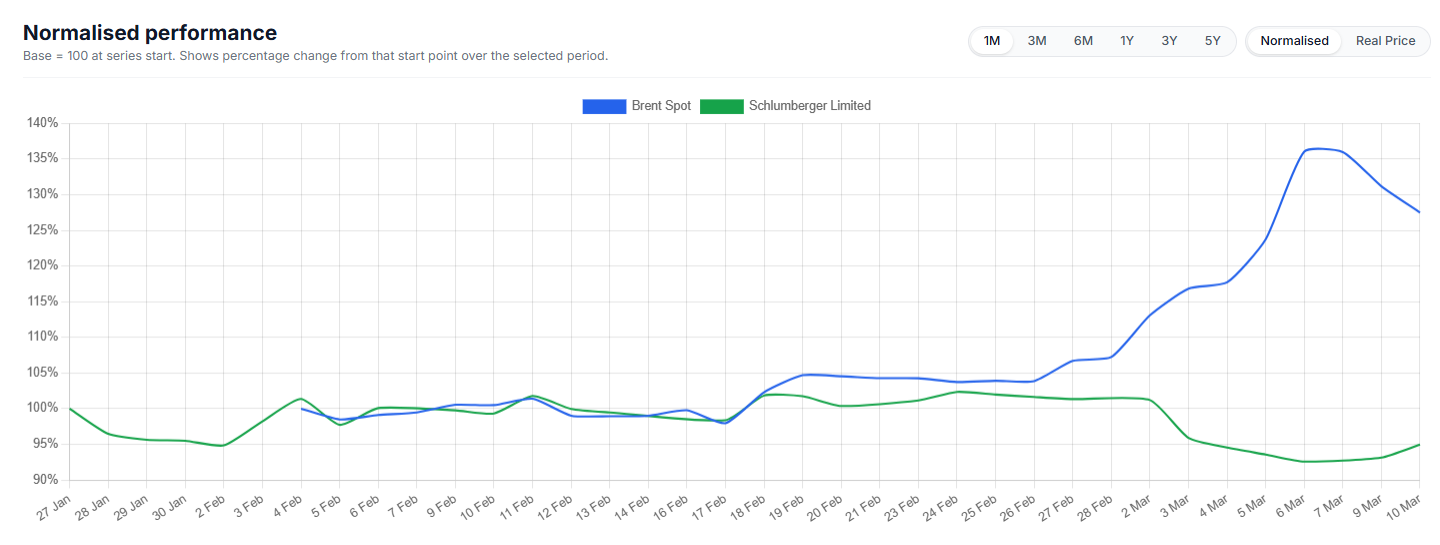

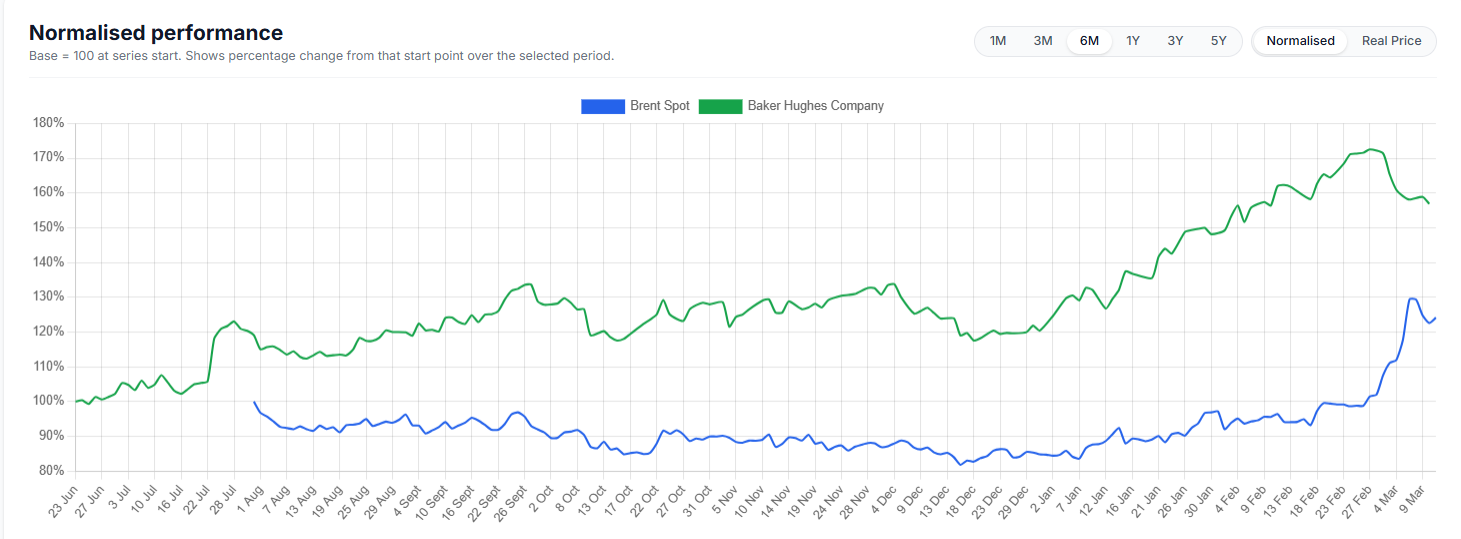

The future earnings of a company can drive up its stock price today because equities discount future earnings to the present. This can explain why oil espoused equities are outperforming spot prices. The spot market does not look as far ahead.

Recent Market Reaction: The sharp negative reaction to OPEC's recent production decision seems irrational in light of the projected tightening of the oil market. The analysis indicates that crude oil inventory draws could reach up to 2 million barrels per day (mb/d) during the third quarter (3Q), suggesting a tighter market. Despite this, the current market sentiment reflects a different view, possibly driven by shorter-term concerns or overreactions to OPEC's decisions.

Seasonal Considerations: Between May and August, global demand for refined products typically rises by approximately 3.2 million barrels per day (mb/d). A similar increase is expected for 2024, driven by seasonal factors. Fundamentals assume oil prices reflect the expected supply/demand balance about 2-3 months into the future.

With that in mind, and looking at demand history Brent might have found a floor in the high-$70s per barrel range and are likely to recover in the coming months. The front-month Brent future for August delivery, are above July and shows that traders are already factoring in the peak northern summer demand. But, and it’s a big But, unlike last year's northern summer tightness which significantly boosted Brent prices higher-than-expected, inventories have tempered expectations.

Thus, calls for Brent to reach $90 per barrel now appear overly ambitious. With inventories higher than previously anticipated, the short-term forecast has been adjusted downward by $1.5 to $4 per barrel for the coming quarter to $$80-$86 a barrel. Post the northern summer period futures are falling fast as those seasonal demands, turning tailwinds into headwinds.

Previous forecasts already showed a declining price trend post the summer quarter. Considering the anticipated surplus in 2025, Brent prices may struggle to maintain the $80 per barrel mark next year. And this will start to impact not just spot and futures but also equities.

The OPEC dynamic OPEC has extended its production cuts, including additional voluntary cuts, through the end of 3Q. Assuming compliance (watching Iran, Iraq and Venezuela here) OPEC production is expected to remain stable during this period. OPEC is expected to remain proactive in managing production levels.

There is a realistic chance that OPEC will limit the unwinding of production cuts well into 2025, preventing a significant price drop and regulate price extraction. Saudi Arabia is known to want a floor in the price at $85 a barrel. Then there is non-OPEC – a temporary slowdown in non-OPEC supply growth is anticipated due to the timing of new projects.

This is interesting as historically non-OPEC loves to step in and soak up cuts from OPEC but appear to be caught slightly on the hop this time around. Limited production growth is expected through September but will increase into the back half of the year and into 2025 as OPEC holds the line. This push pull between the two groups is likely to see a supply surplus and modelling suggests this will make maintaining Brent prices above $80 per barrel challenging.

A full $5 below the comfort level of OPEC. It suggests that OPEC could step in again and cut supply to drive the price higher. However this is when we would expect smaller nations in the OPEC group to splinter as the impact on them is greater than larger players.

Implications for Market Participants Short-term Traders: Should focus on the anticipated supply-demand balance in the next 2-3 months. The expected tightening in 3Q suggests potential price support or increases in the short term. Be ready for price shifts in September and rapid changes in curve the closer we get to August expiry.

Long-term Investors: Need to consider the broader outlook, including potential seasonal shifts, OPEC's future production decisions, and long-term production growth from non-OPEC countries. Look also to forward earnings estimates, possible consolidations and firms that start to pivot from pure oil exposure. This is gaining momentum at the likes of BP, Shell, Woodside and the like.

The long-term dynamic of oil is really that of structural decline as the world moves to renewables and EVs. This is years away no doubt, but the changes and future earnings impacts are starting now – so be alert. Overall, while immediate market reactions can sometimes seem disconnected from longer-term fundamentals, a nuanced understanding of both short-term and long-term factors is crucial for effective oil market analysis and trade decision-making.

The recent analysis reflects adjustments based on current market conditions and forward projections and we hope this provides a baseline for those of you looking at oil and the tricky trading conditions that are present.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs.